The expanding cost and responsibilities associated with employer-sponsored healthcare

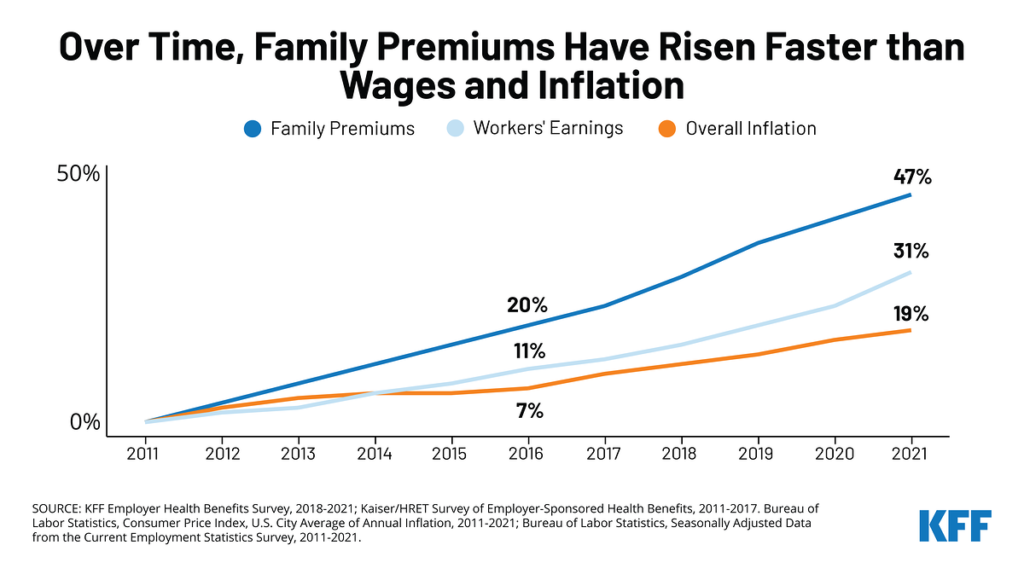

Businesses across the board, from automakers to tech companies to taxpayer-funded school systems, spend a large portion of their budgets on employees in the form of salary and benefits. A rapidly growing percentage of these costs go to fund employee healthcare benefits.1 The expense is significant for both employers and employees. Over the years, employees have been asked to contribute increasingly more toward their own healthcare coverage. As the rising costs of healthcare benefits and the rising percentage of employee contributions converge, companies across America are faced with a new scenario that finds them looking for ways to reduce healthcare spending and protect their employees’ contributions.2

Beyond the dollars

Examining exactly where healthcare dollars are spent is not just a budget management or cost-saving practice for business, as plan sponsors are reminded often, it is also a fiduciary responsibility under the Employee Retirement Income Security Act (ERISA). The U.S. Department of Labor Employee Benefits Security Administration has oversight for the fiduciary duties applicable to employee welfare benefits plans. Under ERISA, employers are accountable for spending employee healthcare contributions as well as the employer’s contributions with the care, skill, and diligence of a prudent person.3 ERISA guidelines for prudent oversight of a health plan are relatively vague, but there are best practices that not only limit fiduciary liability, but also significantly reduce the unnecessary spend in the plan assets.

In comparison to 401(k) benefit plans, historically, very little attention has been given to fiduciary responsibility of health and welfare benefits. This is unfortunate, especially for self-insured employers, because medical plans are ripe for fiduciary liability, mainly from well-recognized waste in the system, according to health benefit compliance expert Brenna A. Davenport. Fiduciaries of medical plans have a duty to mitigate this waste.4

Important lessons can be learned in how employers and 401(k) investment managers have been required to handle 401(k) benefits. According to an Investment News report on 401(k) cases involving fiduciary responsibility, the “minimum requirement is that the appointing fiduciary imposes a regular monitoring procedure.” The report continued that fiduciaries “are required to have procedures in place so that on an ongoing basis they may review and evaluate whether the investment managers are doing an adequate job.”5 There is significant evidence that implementing that same type of ongoing review would be beneficial in healthcare claim payments.

Best practices

Given this weighty responsibility, companies have happily passed on the charge to their plan administrators to prudently act on their behalf in managing plan funds. However, employers tired of year-over-year expense increases are beginning to enlist independent experts to review claims outside of the administrator’s internal process.6 What does best practice of this independent review look like? Best practice is comprised of an independent partner aligned with the plan sponsor on business objectives that has expertise in claims adjudication, analytics, and clinical review of employee health services. Evaluation of the results will confirm if the right partner was chosen to lower costs. Consider these best practices in choosing a “prudent” partner.

Best Practice #1:

Ensure that the claims are being monitored regularly and often. Ideally each claim is reviewed monthly, at a minimum once a quarter. Monthly reviews of post and/or prepay claims allow for immediate intervention, resulting in errors being identified early in the payment process, before overpayments accrue too large. Early identification of errors allows plan administrators to adjust payments to overpaid providers from future remittances, leading to substantial savings and refunds applied towards the plan funds.

Best Practice #2:

Ensure that100% of claims are analyzed using advanced inferential analytic methods. With current software, millions of claims can run through sophisticated scoring models that focus in on the most problematic 10% of claims within a few minutes. Many cost-reduction solutions proclaim review of all claims but in actuality, rely on a finite number of known patterns of wasteful spend or concentrate only on the highest dollar claims. These rules-based methods leave hundreds of thousands, even millions, of avoidable spend unaddressed. In contrast, advanced analytic methods implemented by a knowledgeable team, use data to quickly detect the specific anomalies in the given claims population. Contrary to static rules, inferential analytic models dynamically ad just to different employee populations resulting in 3 to 4 times the savings as traditional algorithms.

Best Practice #3:

Ensure clinical and adjudication expertise is being used to resolve errors in coordination with the plan administrator. Clinical experts can separate scenarios that an analytic model identified as an anomaly but instead are claims from an unusual clinical situation or even bad data. These scenarios, referred to as “false positives”, can result in wasted time and money if not weeded out prior to taking action. Analytic models label a claim as an error based on predictive attributes. However, even the most robust models are only 50-70% accurate in predicting true overpayments. Additional expert review, when done well, can significantly raise the confidence level that an overpayment exists.

Best Practice #4:

Avoid inherent conflicts of interest in selecting service providers. Relying on the same entity to process the claims and also notify plan sponsors when they themselves have made a mistake, introduces a substancial conflict of interest. Large or small third-party administrators (“TPA”) are obligated to provide the best service to thousands of clients at once. The claims from any single employer can get lost in the millions of members’ claims processed each year. 7

Best Practice #5:

Ensure the chosen service provider is effective. Studies show that roughly 10% of healthcare payments are wasted because of intentional fraud, abuse, and unintentional errors.8 A committed service provider following best practice guidelines is expected to not merely identify but also eliminate 3-5% of the plan costs attributed to waste, with minimal member disruption. An effective service provider should mitigate errors in the claims data each month. The errors identified should be made transparent (without compromising protected health information) and the subsequent overpayments stopped within a reasonable time period. The ideal partner should prove their worth many times over through consistent tracking against success outcome measures. Value-driven, committed service providers would welcome objective measurements of success.

Under ERISA, the investment of plan assets is a fiduciary act governed by the fiduciary standards in ERISA section

Office of the Federal Register National Archives

40-f(a)(l)(A) and (B), which require plm1 fiduciaries to act prudently and solely in the interest of the plan’s participants and beneficiaries

Having an independent expert consistently monitoring claim payments and applying best practices ensures that a company meets its “prudent person” requirement, while also reducing the cost of employee healthcare. A fundamental requirement to implement best practices are that the plan sponsor maintains control over who has access to their employees paid claims data and that the administrative services agreement allows for sensible oversight on the professional services purchased. Since plan sponsors are mandated to monitor and safeguard plan assets under ERISA, entering into an agreement that intentionally muddles payment details could arguably undermine ERISA fiduciary duty provisions.9

Case Studies

Case Study #1:

Company A contracts with one administrator to process its medical benefits and a separate administrator to handle behavioral health claims. An employee seeks care from a medical provider who erroneously (intentionally or unintentionally) submits the claims for treatment to both the medical administrator and to the behavioral health administrator. Neither administrator is aware of the other’s payment for the single member visit, consequently, the provider is paid twice for the same service, once from each administrator.

Monthly monitoring by an independent, cost-reduction partner who receives data feeds from both sources identifies the duplicate payment and determines that only the behavioral health claim was appropriate. The medical administrator is alerted to the issue and refunds the payment back to the employer, which unwittingly paid twice for the single service. This specific instance occurred monthly, quickly adding dollars to the waste in the employer’s healthcare spend.

Analysis

In this case, neither of the administrators, nor the employer or employee is aware of the duplicate payment. Only the physician could know that he was erroneously paid twice. If aware, he could proactively take measures to return the duplicate payment to one of the carriers, but whether intentional or due to the complexities of administering thousands of patients, this is rarely the reality. Only an independent reviewer has the capability and the motive to eliminate the duplicate payment. In this case study, a standard random sample audit would consider both claim payments as “accurate.”

Case Study #2

An in-network provider uses a commonly covered procedure code to bill for an investigational and noncovered treatment. Misrepresenting non-covered codes as a covered service is a common abusive billing pattern.10 In this case, sublingual hormone drops, which are not a covered service, were being used to promote anti-aging and billed as common allergy procedures. The supporting data and contextual evidence were discussed with the administrator who stopped subsequently submitted claims and prevented future losses. As in the previous case, since records did not support valid medical services, these payments were later denied, and the payment errors credited back to the plan funds.

Analysis

Inferential analytics was used to model “normal” behavior for the specified provider peer group. Those providers whose billing pattern warrants additional scrutiny are referred for payment error validation and subsequent claim denials, if appropriate.

Too many employers willingly hand over supervision of their plan funds to their claims administrators, assuming the complex decisions of providing healthcare are best managed by those whose business it is to process the payments. However, such a delegation does not release the plan administrator from liability. Even if employers hire third-party service providers, they are still duty-bound to monitor the payments made from their plan funds.11 Incorporating independent expertise that follow best practice guide lines to ensure efficient management of the health plan is the prudent step forward.

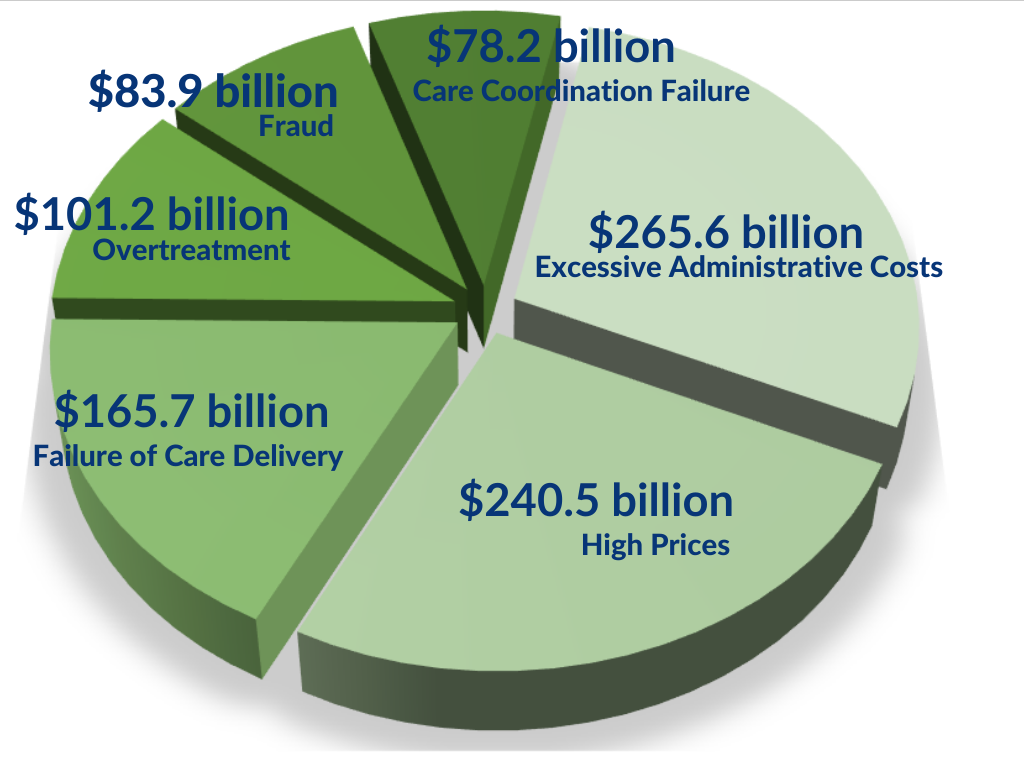

Waste in Healthcare 2019*

The How

Healthcare claim analysis specialists with years of clinical experience can review claims with minimal disruption to claims processing. Such experts do not need to touch each and every claim to find the errors; instead, using their expertise in inferential analytics, they predict which claims have the highest probability of being an overpayment due to unnecessary procedures, units or other factors that drive up costs. Every claim does not have the same chance of being an overpayment. The methods used to identify which claims should be stopped for additional inspection and which should be processed immediately depends on specific characteristics of the claim and its context. Proprietary models that combine clinical context with mathematical anomalies have proven to be the most effective at pinpointing “true positive” wasteful payments.

The issue boils down to this: Benefits are a recruiting and retention tool for employers – and in any successful business, resources need to be spent wisely. It behooves a company to not only provide the highest quality benefits overall, but to make sure the money invested on health benefits is not wasted unnecessarily on billing errors, abusive use of the emergency department, testing for medically unlikely scenarios, or on intentional fraud.

In October 2019, the Washington Health Alliance (WHA) issued a report that examined waste in commercially insured and Medicare-insured individuals. The report evaluated 47 common treatments with a total estimated spend of $703 million. More than half – 51% – of the measured services were found to have minimal clinical value, simply put, were wasteful.The WHA titled the report “First Do No Harm” based on the medical field’s long-standing ethical principle. The report went on to say, that in addition to doing no physical harm, there is also a responsibility to do no financial harm when providing employee healthcare benefits.12

The good news for employers is that selective prudent oversight of healtcare claims allows employers to provide benefits to employees at a lower cost while also enabling them to carry out their fiduciary responsibility and simultaneously maintain their focus on building cars, developing software, or providing education.

REFERENCES

- Alliance for Health Policy. The Sourcebook: Essentials of Health Policy. Chapter 5 – Health Care Costs. August 31, 2017.

- SHRM. “For 2019, Employers Adjust Health Benefits as Costs Near $15,000 per Employee”. Stephen Miller. August 13, 2018.

- U.S. Department of Labor. Understanding Your Fiduciary Responsibilities Under aGroup Health Plan. September 2015.

- United States: Fiduciary Responsibility…You Mean That Stuff Applies to the Health Plan I Sponsor Too? Brenna A. Davenport. June 14, 2017.

- lnvestmentNews. “Appointing and monitoring a 401(k) investment manager under ERISA’’. Marcia Wagner. July13, 2017.

- Forbes. “Three Strategies For HR Leaders To Combat Rising Healthcare Costs”. Heather Halliburton. December 18, 2018.

- BlueCross BlueShield Association.”Blue Facts”. May 2018.

- Health Affairs. “Wasted Health Spending: Who’s Picking Up The Tab?”. Daniel O’Neill and David Scheinker. May 31, 2018.

- American Health Policy Institute. “ERISA Fiduciary Responsibilities for Health Care Plans”. 2018.

- ACFE. “10 popular health care provider fraud schemes”. Charles Piper.January/February 2013.

- Forbes. “CFOs And HR Execs Facing Millions In Liability Due to Unmanaged Health Benefits Plans”. Dave Chase. May 26, 2016.

- Washington Health Alliance. “First, Do No Harm Calculating Health Care Waste inWashington State”. October 2019.

ADDITIONAL WORK CONSULTED/SOURCE READING

Kaiser Family Foundation 2021 Employer Health Benefits Survey

Would you like a copy of this paper? Click here.